Unit 4 - Imperfect Competition

Printable Cheat Sheets for Units 1–5

Single-page PDFs for Units 1-5. The full unit experience for Unit 6 stays on this cheat sheet page.

Download PDF Cheat SheetsTable of Contents

Built into this unit

Flashcards

30 cards mix graphs, formulas, and key terms. Shuffle blends every type so you drill the whole unit—not just one format.

4.1 - Introduction to Imperfectly Competitive Markets

Key Terms & Definitions

Imperfect Competition

A market structure that fails to meet the conditions of perfect competition, where firms have some control over the price.

- •Includes Monopoly, Oligopoly, and Monopolistic Competition.

- •Firms are "Price Makers" rather than "Price Takers".

- •The Demand curve for the firm is downward sloping.

4.2 - Monopoly

Monopoly

Learn about monopoly markets, barriers to entry, and profit maximization for a monopolist.

Key Terms & Definitions

Monopoly

A market structure where there is only one large firm (the firm is the market) producing a unique product.

- •Characteristics: High barriers to entry, "price makers".

- •Marginal Revenue (MR) is less than Demand (Price).

- •There are no close substitutes for the good.

Marginal Revenue in Monopoly

The additional revenue from selling one more unit. In a monopoly, the MR curve lies below the Demand curve.

- •To sell more units, the firm must lower the price on ALL units sold, not just the last one.

- •MR < Price at every quantity after the first unit.

Elasticity and Total Revenue (Monopoly)

A monopoly will only produce in the elastic range of the demand curve.

- •Elastic Range: MR > 0. Total Revenue increases as Price decreases.

- •Inelastic Range: MR < 0. Total Revenue decreases as Price decreases.

- •Total Revenue is maximized where MR = 0 (Unit Elastic).

Inefficiency of Monopoly

Monopolies are inefficient because they charge a higher price and produce a lower quantity than perfectly competitive markets.

- •Allocatively Inefficient: Price > Marginal Cost (P > MC).

- •Productive Inefficient: Price > Minimum ATC.

- •Creates Deadweight Loss (DWL).

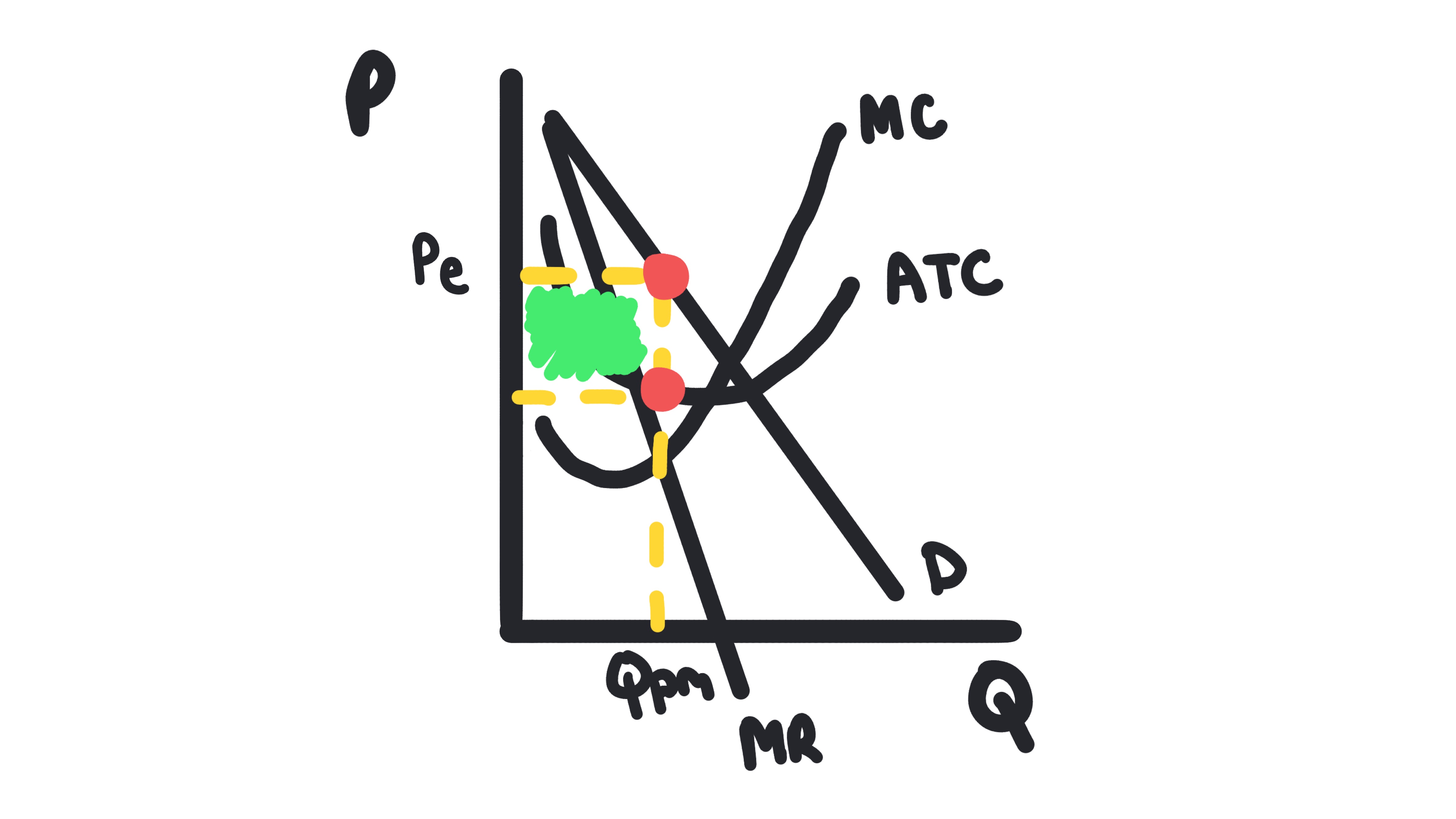

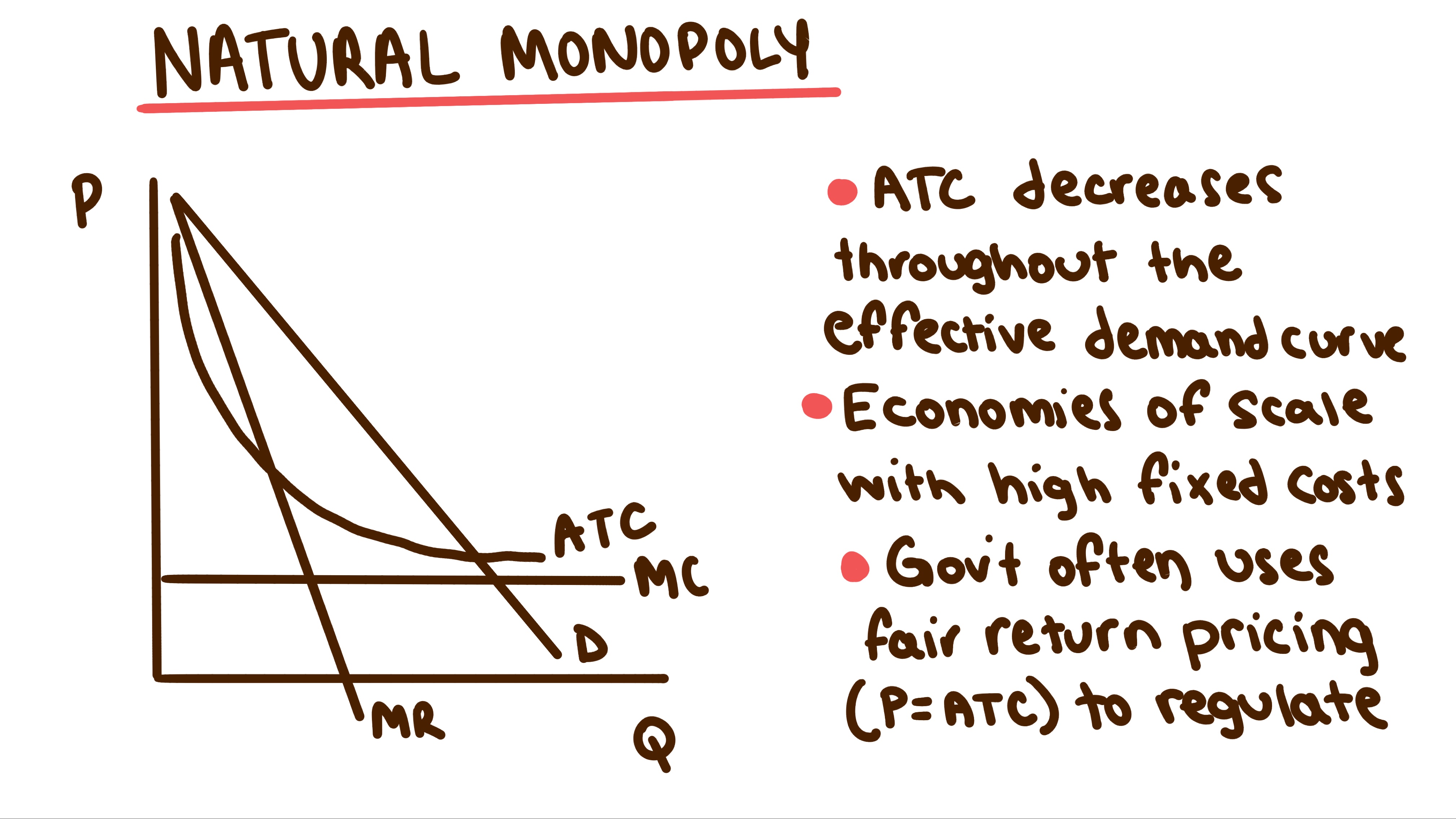

Natural Monopoly

A market structure where a single firm can supply a good or service more efficiently than multiple competitors as a result of high start-up costs and general economies of scale.

- •ATC decreases across the entire range of the effective demand curve.

Regulating Monopolies

Government price controls used to reduce the inefficiency of natural monopolies.

- •Socially Optimal Price: Set P = MC (Allocative Efficiency). May cause a loss for the firm.

- •Fair Return Price: Set P = ATC (Normal Profit). Firm breaks even.

Whiteboards

4.3 - Price Discrimination

Price Discrimination

Learn about price discrimination, conditions required for it, and its effects on consumer and producer surplus.

Key Terms & Definitions

Price Discrimination

The practice of selling the same product to different buyers at different prices based on their willingness to pay.

- •Conditions: Firm must have market power, be able to segregate the market, and prevent resale.

- •Result: Converts Consumer Surplus into Profit.

- •Perfect Price Discrimination: MR = Demand. No Deadweight Loss. Allocatively Efficient.

4.4 - Monopolistic Competition

Monopolistic Competition

Learn about monopolistically competitive markets, product differentiation, and long-run equilibrium.

Key Terms & Definitions

Monopolistic Competition

A market structure with many sellers offering differentiated products.

- •Characteristics: Relatively large number of sellers, easy entry and exit, non-price competition (advertising).

- •Products are substitutes but not identical (e.g., fast food, furniture).

Product Differentiation

Strategies used by firms to distinguish their products from competitors, such as branding, quality, or features.

- •Gives the firm some control over price (Demand is downward sloping but highly elastic).

Long-Run Equilibrium (Monopolistic Competition)

In the long run, firms enter or exit until economic profit is zero.

- •Entry/Exit shifts the Demand curve.

- •Equilibrium: Price = ATC (Normal Profit), but Price > MC (Inefficient).

- •Demand is tangent to the ATC curve.

Excess Capacity

The gap between the minimum ATC output and the profit-maximizing output.

- •The firm could produce at a lower cost but holds back production to maximize profit.

4.5 - Oligopoly and Game Theory

Oligopoly and Game Theory

Learn about oligopoly, interdependence between firms, and game theory strategies.

Key Terms & Definitions

Oligopoly

A market structure dominated by a few large producers.

- •Characteristics: High barriers to entry, identical or differentiated products.

- •Key Feature: Mutual Interdependence (decisions depend on competitors).

Game Theory

The study of how people/firms behave in strategic situations.

- •Used to analyze the pricing and output decisions of oligopolies.

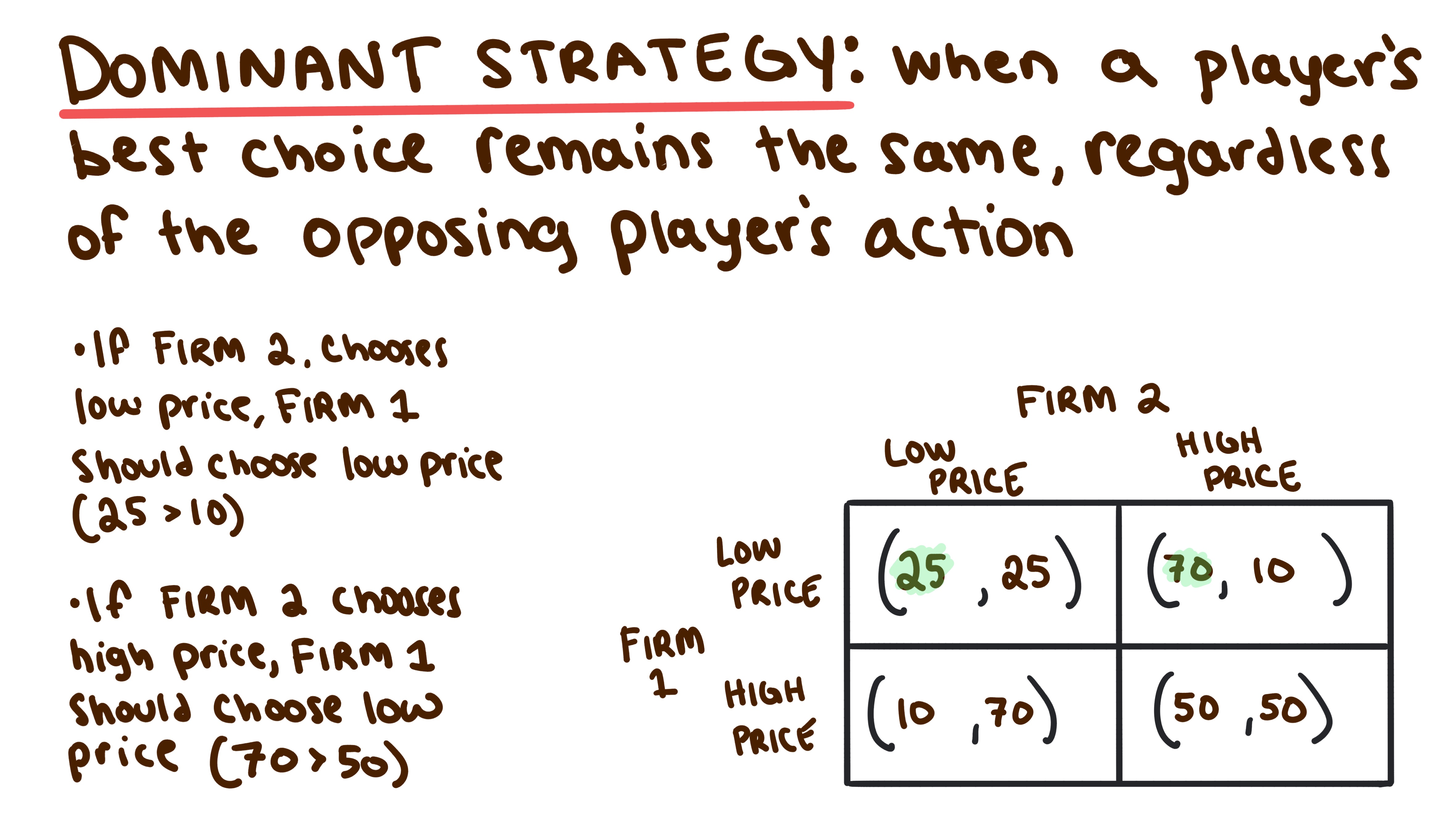

Dominant Strategy

The best move to make regardless of what your opponent does.

- •Not all games have a dominant strategy.

- •How to identify:

- •For Player 1: Check each row - if one row has higher payoffs than another in every column, that row is dominant.

- •For Player 2: Check each column - if one column has higher payoffs than another in every row, that column is dominant.

- •A strategy is dominant if it yields a better payoff than all other strategies, regardless of opponent's choice.

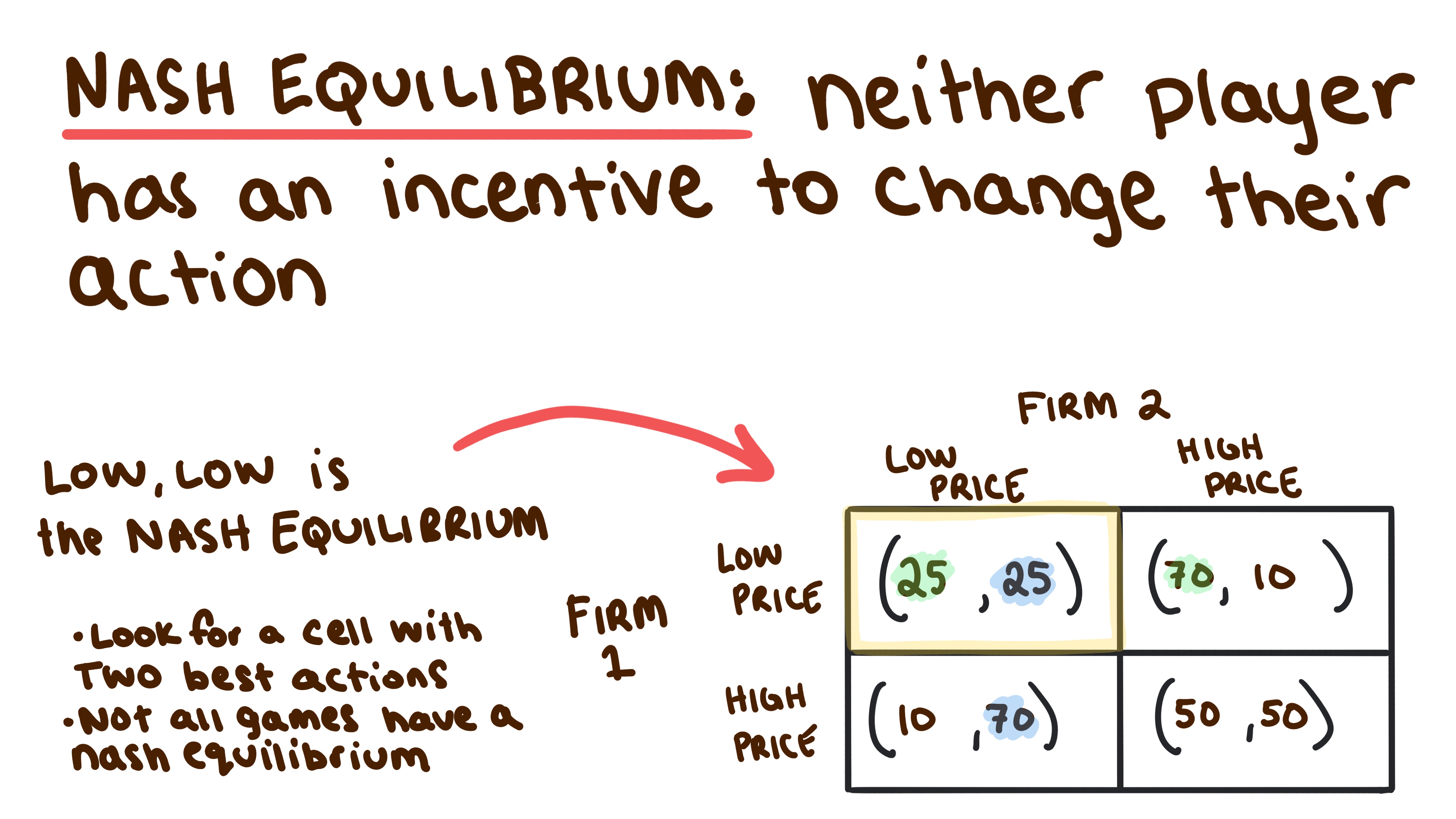

Nash Equilibrium

The outcome that occurs when both firms make decisions simultaneously and have no incentive to change.

- •The "optimal" outcome given the rival's choice.

- •How to identify:

- •Step 1: For each cell, check if Player 1's payoff is the highest in that column (best response to Player 2's strategy).

- •Step 2: For the same cell, check if Player 2's payoff is the highest in that row (best response to Player 1's strategy).

- •If both conditions are true, that cell is a Nash equilibrium.

- •A Nash equilibrium can exist even if neither player has a dominant strategy.

Collusion / Cartel

A group of producers that create an agreement to fix prices high, effectively acting as a monopoly.

- •They restrict output to maximize collective profit.

- •Cartels are unstable because firms have an incentive to cheat (lower price) to gain market share.

Whiteboards