Unit 5 - Factor Markets

Printable Cheat Sheets for Units 1–5

Single-page PDFs for Units 1-5. The full unit experience for Unit 6 stays on this cheat sheet page.

Download PDF Cheat SheetsTable of Contents

Built into this unit

Flashcards

25 cards mix graphs, formulas, and key terms. Shuffle blends every type so you drill the whole unit—not just one format.

5.1 - Introduction to Factor Markets

Introduction to Factor Markets

Learn about factor markets, derived demand, and how firms hire resources.

Key Terms & Definitions

Factors of Production

The resources used to produce goods and services: Land, Labor, Capital, and Entrepreneurship.

- •Labor: Human effort used in production (wages).

- •Land: Natural resources (rent).

- •Capital: Tools and machinery (interest).

- •Entrepreneurship: Risk-taking and innovation (profit).

Factor Market

The market where the factors of production (resources) are bought and sold.

- •Households supply resources (Supply curve).

- •Firms demand resources (Demand curve).

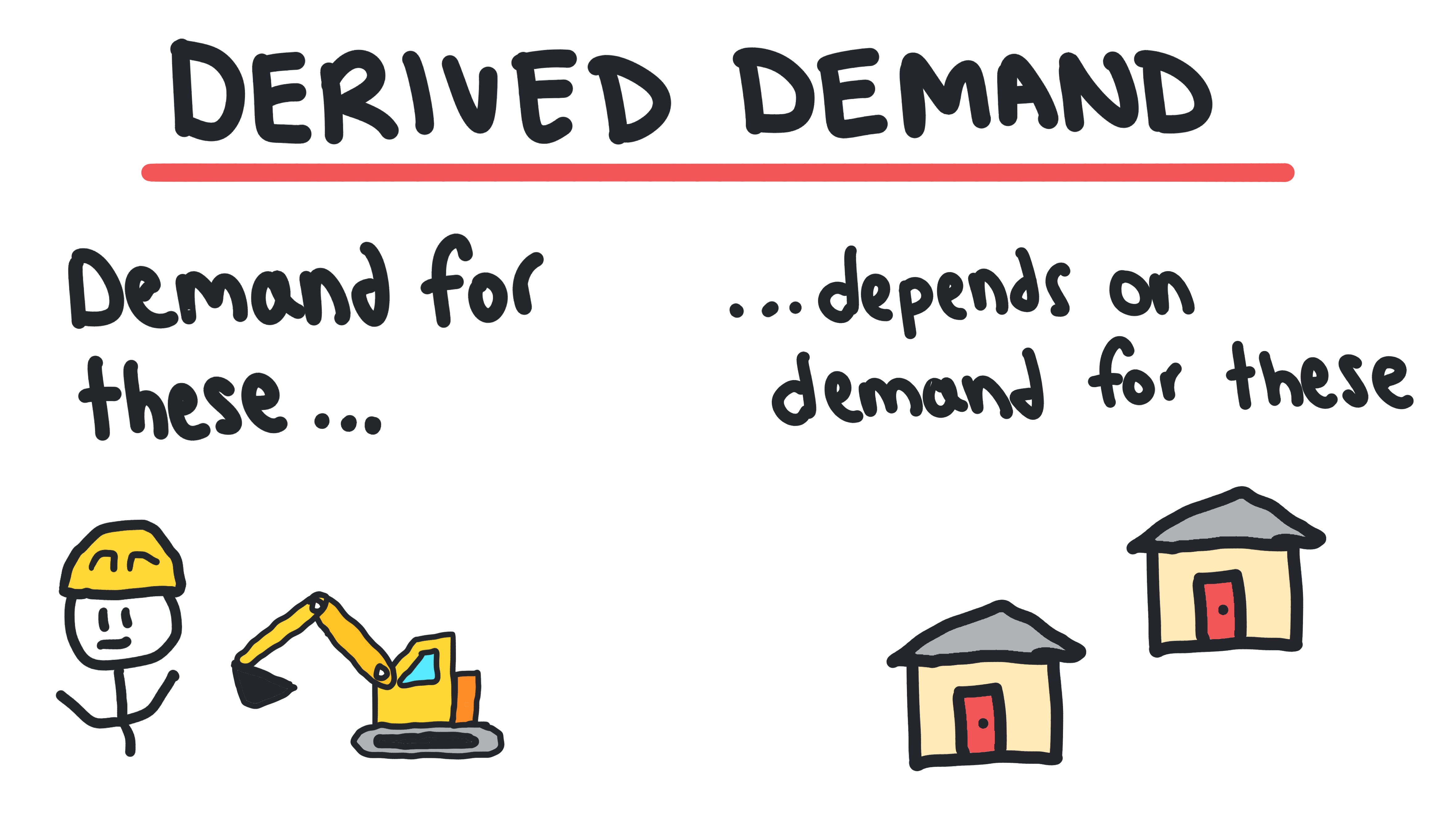

Derived Demand

The concept that the demand for a resource is determined by the demand for the good or service that resource produces.

- •If the demand for pizza goes up, the demand for pizza chefs goes up.

- •Resource demand is NOT independent.

Labor Supply

The relationship between the wage rate and the quantity of labor that households are willing and able to provide.

- •Households are responsible for labor supply.

- •There is a direct relationship between the wage rate and the quantity of labor supplied.

- •A change in the wage rate leads to a change in the quantity of labor supplied (Qs).

Labor Demand

The relationship between the wage rate and the quantity of labor that firms are willing and able to hire.

- •Firms are responsible for labor demand.

- •There is an inverse relationship between the wage rate and the quantity of labor demanded.

- •A change in the wage rate leads to a change in the quantity of labor demanded (Qd).

Whiteboards

5.2 - Changes in Factor Demand and Factor Supply

Key Terms & Definitions

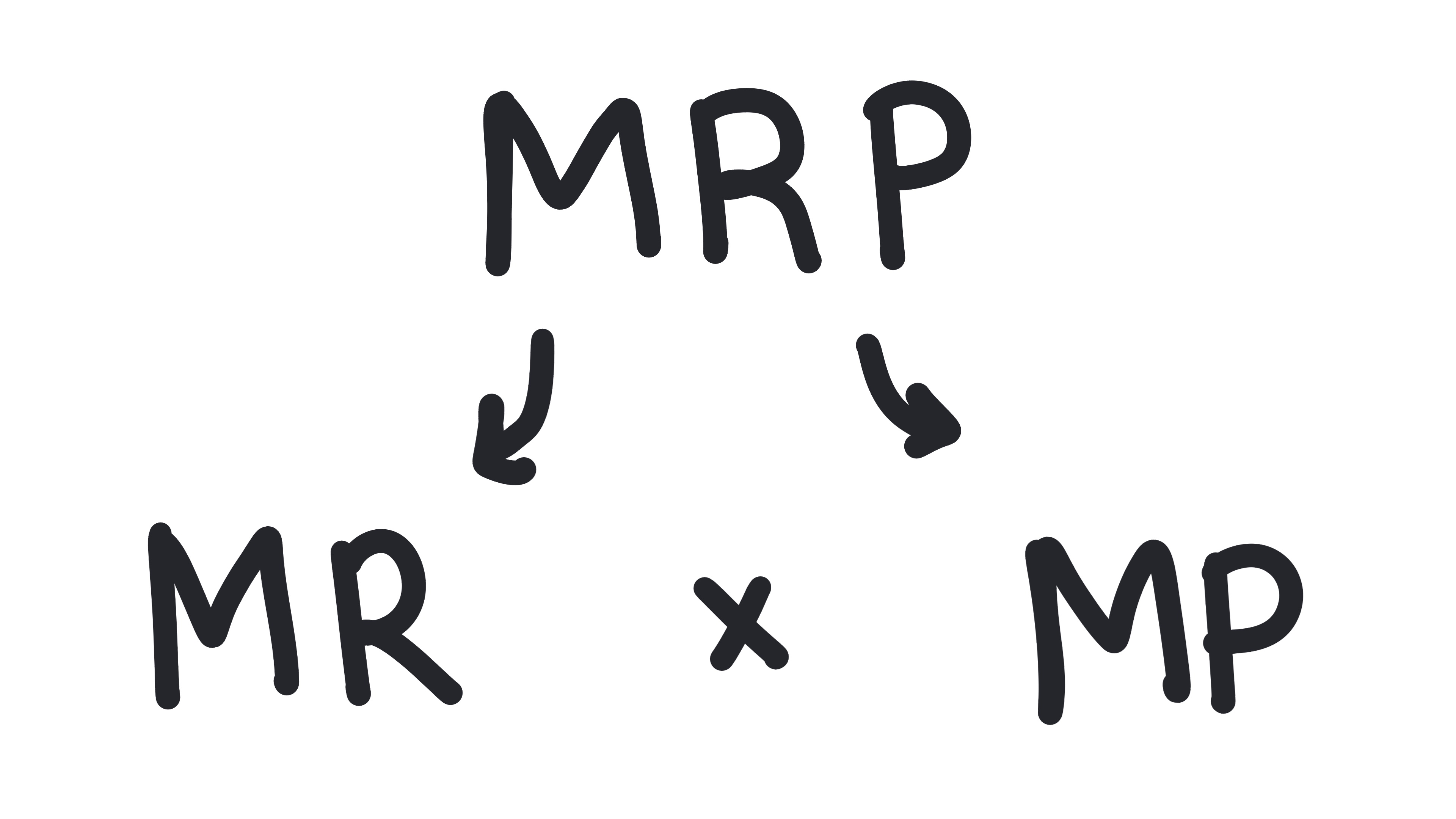

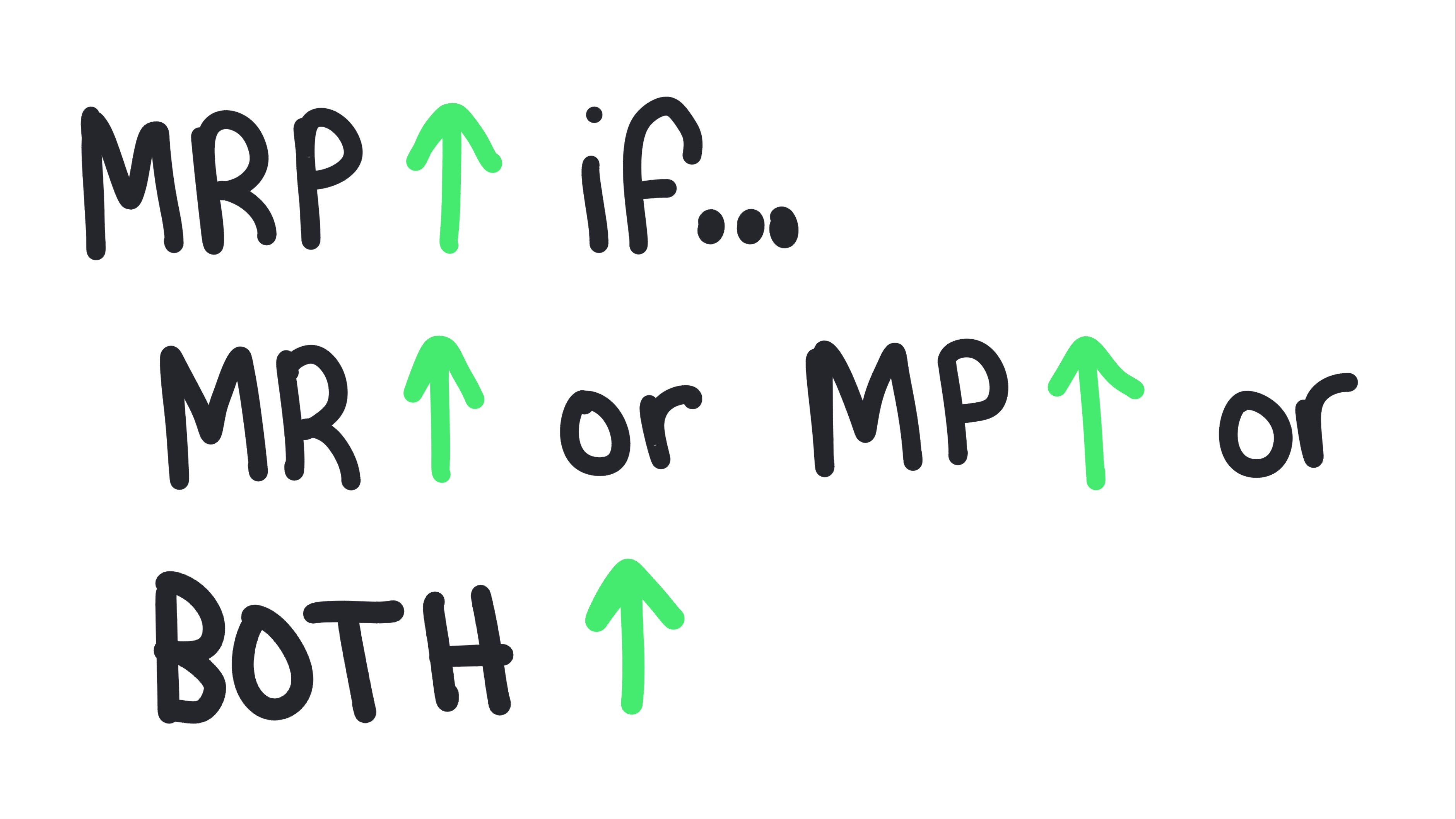

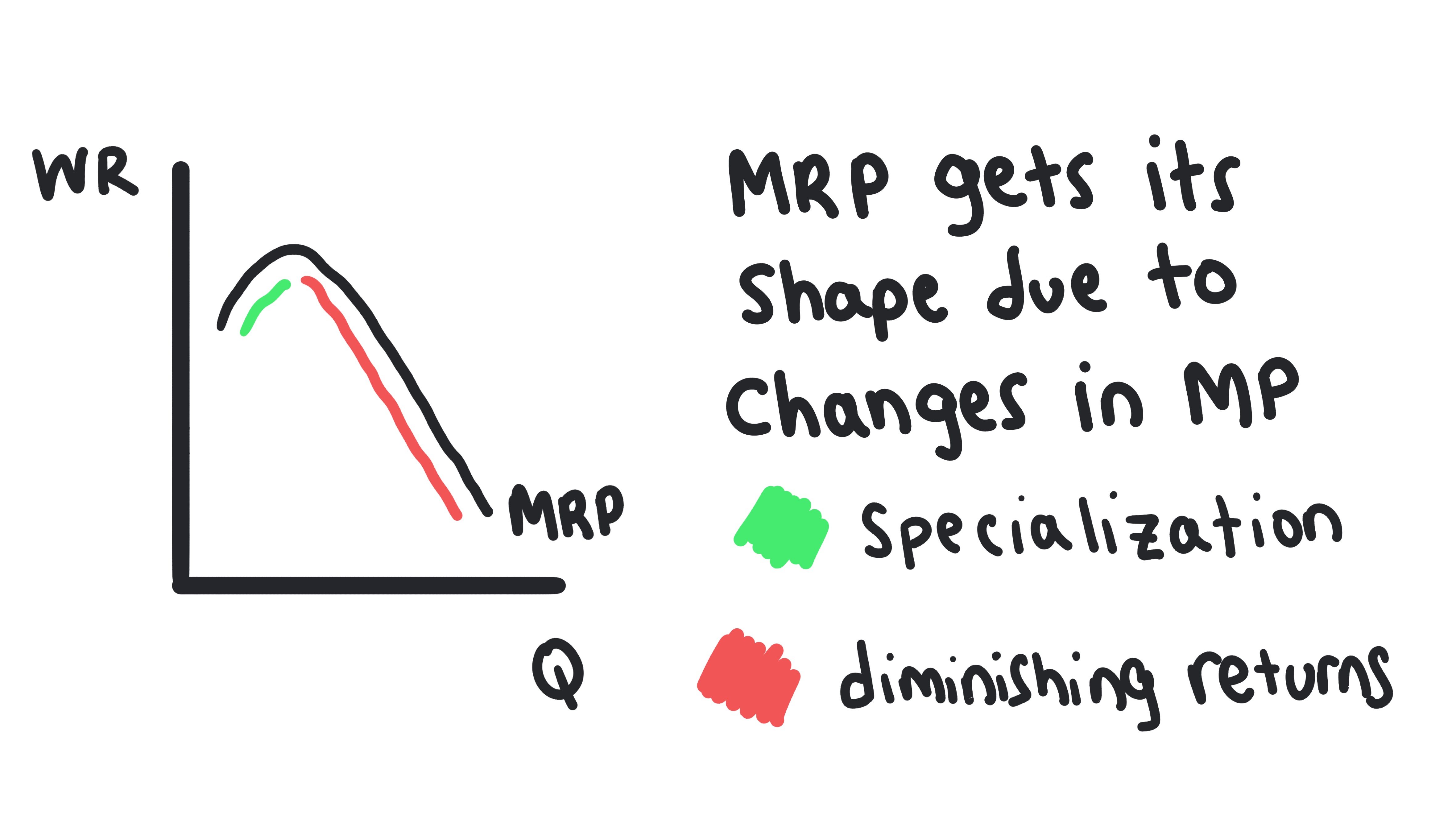

Marginal Revenue Product (MRP)

The additional revenue generated by hiring one more unit of a resource (e.g., one more worker).

- •Formula: Marginal Product (MP) x Marginal Revenue (MR).

- •Represents the Factor Demand Curve for the firm.

Marginal Factor Cost (MFC)

The additional cost incurred by hiring one more unit of a resource.

- •Also known as Marginal Resource Cost (MRC).

- •Formula: Change in Total Resource Cost / Change in Quantity of Resource.

- •In a perfectly competitive labor market, MFC equals the Wage.

Shifters of Labor Demand

Factors that shift the MRP curve (Demand for Labor).

- •Change in Price of the Product (P↑ → MRP↑).

- •Change in Productivity (MP↑ → MRP↑).

- •Change in Price of Related Resources (Substitutes/Complements).

Shifters of Labor Supply

Factors that shift the supply of labor curve.

- •Education and Training.

- •Availability of alternative opportunities.

- •Migration and Population changes.

- •Changes in leisure preferences.

Whiteboards

5.3 - Profit-Maximizing Behavior in Perfectly Competitive Factor Markets

Profit-Maximizing Behavior in Perfectly Competitive Factor Markets

Learn how firms hire labor and other resources in perfectly competitive factor markets to maximize profit.

Key Terms & Definitions

Marginal Revenue Product (MRP)

The additional revenue generated by hiring one more unit of a resource (e.g., one more worker).

- •Formula: Marginal Product (MP) x Marginal Revenue (MR).

- •Represents the Factor Demand Curve for the firm.

Marginal Factor Cost (MFC)

The additional cost incurred by hiring one more unit of a resource.

- •Also known as Marginal Resource Cost (MRC).

- •Formula: Change in Total Resource Cost / Change in Quantity of Resource.

- •In a perfectly competitive labor market, MFC equals the Wage.

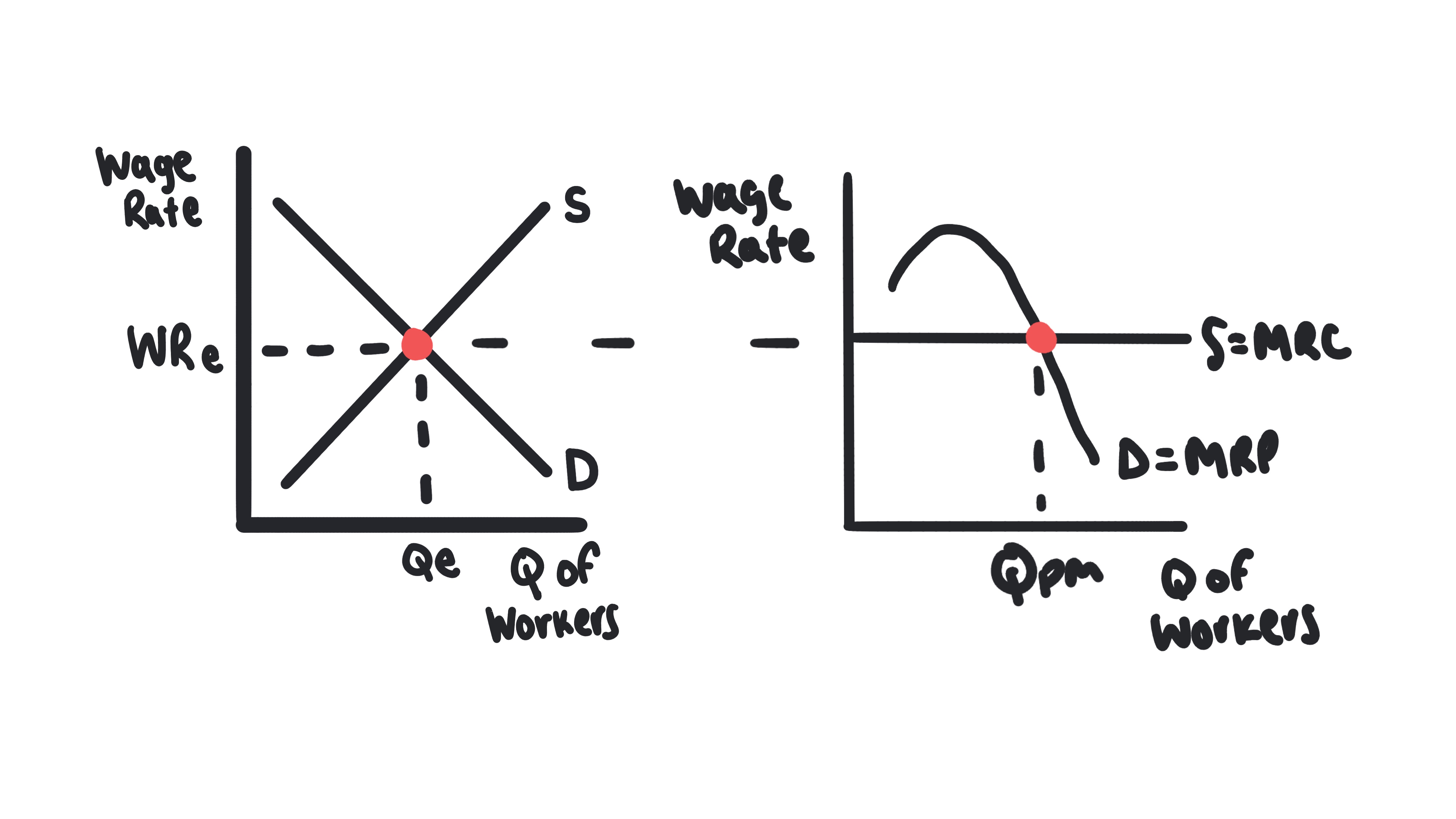

Profit-Maximizing Hiring Rule

A firm should continue to hire resources as long as the additional revenue brought in by the resource is greater than or equal to the additional cost.

- •Formula: Hire where MRP = MFC (or MRP = MRC).

- •Works just like MR = MC for output.

Perfectly Competitive Labor Market

A labor market with many small firms hiring, many workers with identical skills, and constant wages.

- •Firms are "Wage Takers".

- •The firm's supply of labor is perfectly elastic (horizontal) at the market wage.

Least-Cost Rule (Cost Minimization)

The optimal combination of two different resources (like Labor and Capital) to produce a specific output at the lowest cost.

- •Formula: (MP of Labor / Price of Labor) = (MP of Capital / Price of Capital).

- •Basically, get the same "bang for your buck" from the last dollar spent on each resource.

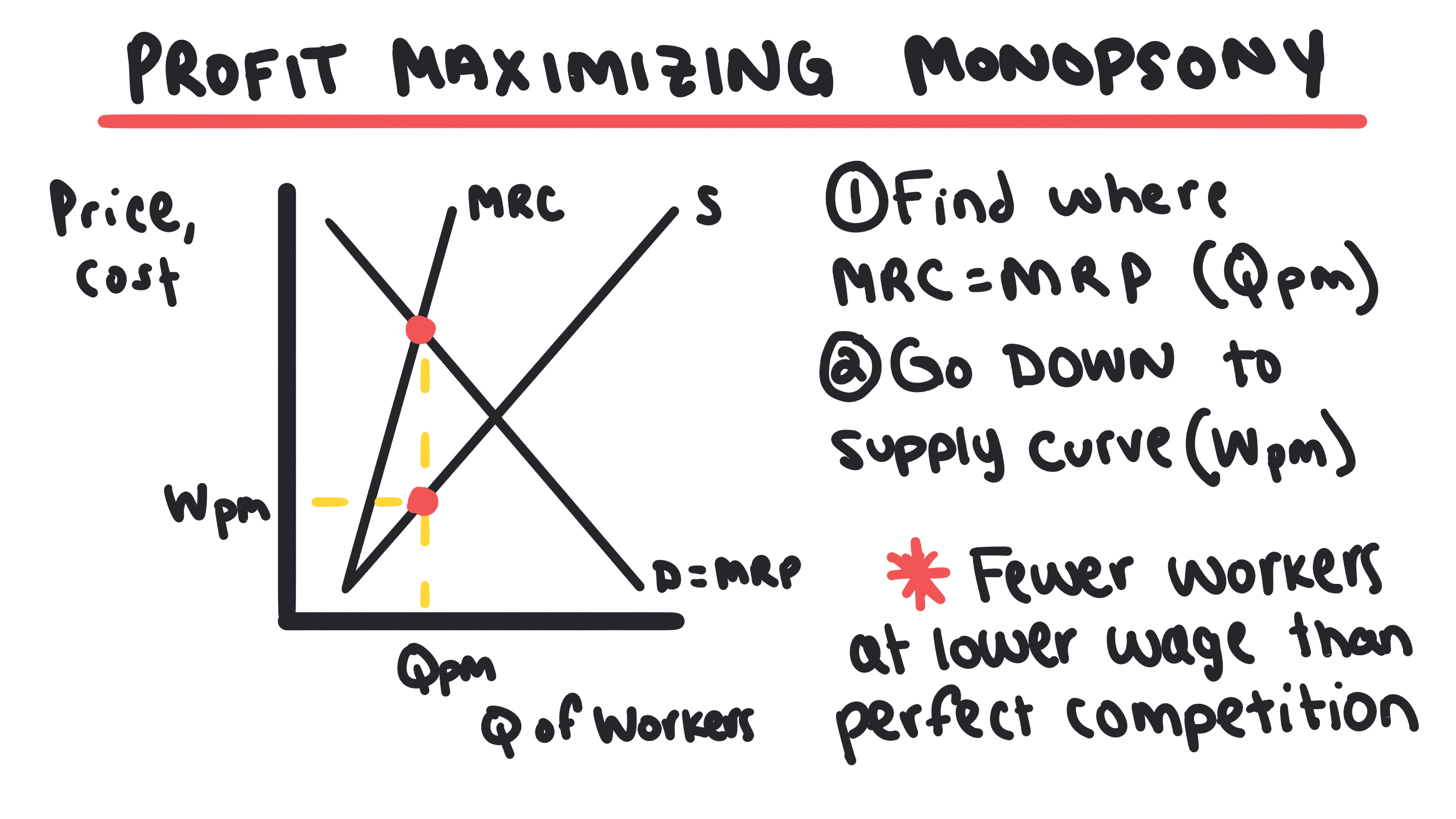

5.4 - Monopsonistic Markets

Monopsonistic Markets

Learn about monopsony, wage determination, and inefficiency in labor markets with a single buyer.

Key Terms & Definitions

Monopsony

A market structure where there is only a single buyer of a resource (e.g., a "company town" where one factory hires everyone).

- •The firm is a "Wage Maker".

- •To hire more workers, the firm must raise the wage for ALL workers, not just the new one.

Monopsony Graphing

In a monopsony, the Marginal Factor Cost (MFC) curve lies above the Supply curve.

- •The MFC curve lies above the Supply curve because in a monopsony, to hire one more worker, the firm must raise the wage for ALL workers, not just the new one.

- •Example: If a firm currently pays 11/hour for all 11 workers. The MFC of the 11th worker is 10 (the additional 21, which is above the $11 supply price.

- •Quantity hired is determined where MRP = MFC.

- •Wage paid is determined by the Supply curve at that quantity (Wage < MRP).

- •Result: Monopsonies hire fewer workers and pay lower wages than competitive markets.

Whiteboards