Unit 4 - Imperfect Competition

Table of Contents

4.1 - Introduction to Imperfectly Competitive Markets

Key Terms & Definitions

Imperfect Competition

A market structure that fails to meet the conditions of perfect competition, where firms have some control over the price.

- •Includes Monopoly, Oligopoly, and Monopolistic Competition.

- •Firms are "Price Makers" rather than "Price Takers".

- •The Demand curve for the firm is downward sloping.

4.2 - Monopoly

Key Terms & Definitions

Monopoly

A market structure where there is only one large firm (the firm is the market) producing a unique product.

- •Characteristics: High barriers to entry, "price makers".

- •Marginal Revenue (MR) is less than Demand (Price).

- •There are no close substitutes for the good.

Marginal Revenue in Monopoly

The additional revenue from selling one more unit. In a monopoly, the MR curve lies below the Demand curve.

- •To sell more units, the firm must lower the price on ALL units sold, not just the last one.

- •MR < Price at every quantity after the first unit.

Elasticity and Total Revenue (Monopoly)

A monopoly will only produce in the elastic range of the demand curve.

- •Elastic Range: MR > 0. Total Revenue increases as Price decreases.

- •Inelastic Range: MR < 0. Total Revenue decreases as Price decreases.

- •Total Revenue is maximized where MR = 0 (Unit Elastic).

Inefficiency of Monopoly

Monopolies are inefficient because they charge a higher price and produce a lower quantity than perfectly competitive markets.

- •Allocatively Inefficient: Price > Marginal Cost (P > MC).

- •Productive Inefficient: Price > Minimum ATC.

- •Creates Deadweight Loss (DWL).

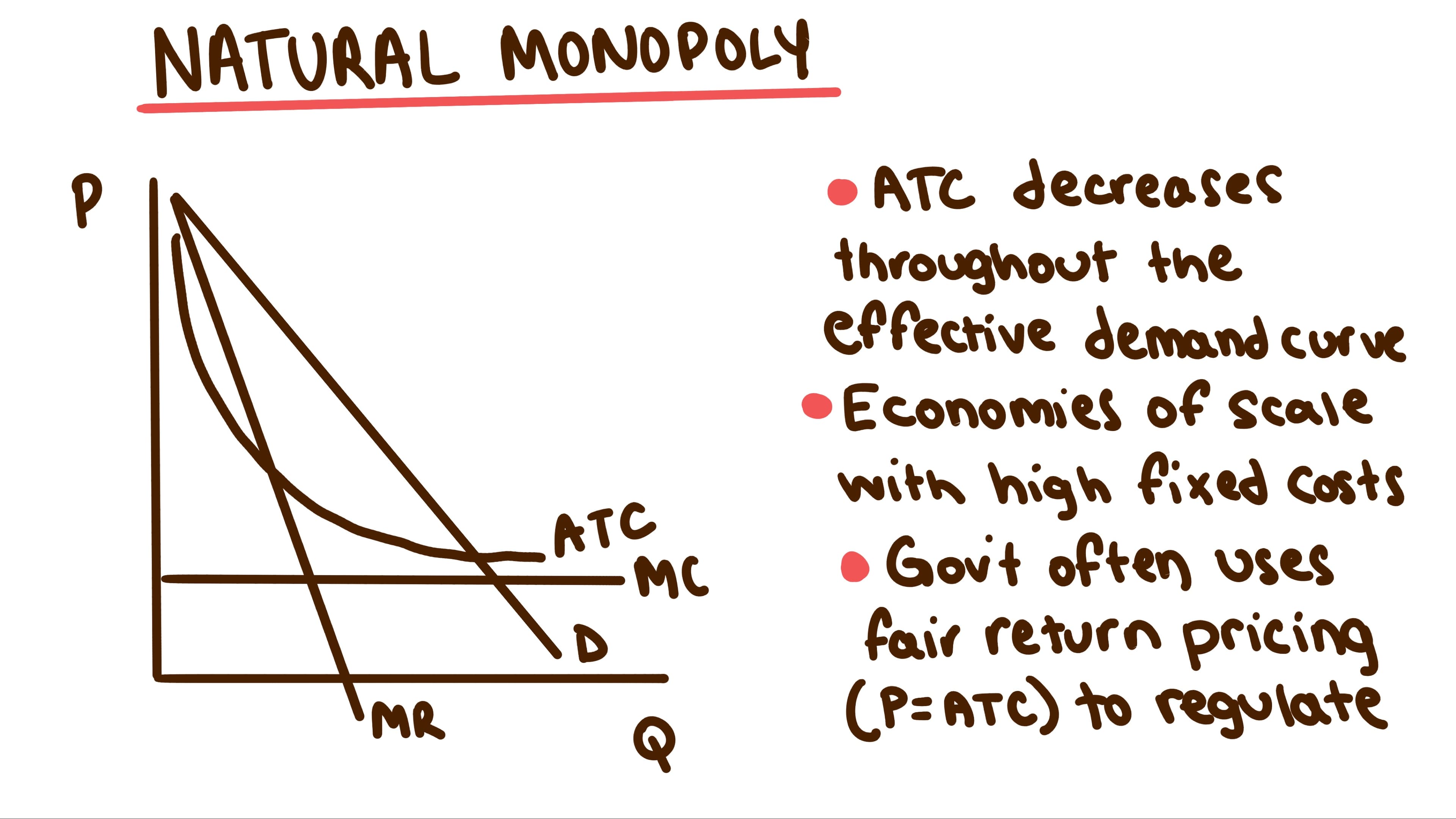

Natural Monopoly

A distinct type of monopoly where one firm can produce the socially optimal quantity at the lowest cost due to economies of scale.

- •The ATC curve falls over the relevant range of production.

- •It is better to have one firm because two firms would have higher average costs.

Regulating Monopolies

Government price controls used to reduce the inefficiency of natural monopolies.

- •Socially Optimal Price: Set P = MC (Allocative Efficiency). May cause a loss for the firm.

- •Fair Return Price: Set P = ATC (Normal Profit). Firm breaks even.

Whiteboards

4.3 - Price Discrimination

Key Terms & Definitions

Price Discrimination

The practice of selling the same product to different buyers at different prices based on their willingness to pay.

- •Conditions: Firm must have market power, be able to segregate the market, and prevent resale.

- •Result: Converts Consumer Surplus into Profit.

- •Perfect Price Discrimination: MR = Demand. No Deadweight Loss. Allocatively Efficient.

Checkpoint

Test your understanding of 4.1

Imperfectly competitive markets are characterized by:

Checkpoint

Test your understanding of 4.2

A monopolist produces where:

4.4 - Monopolistic Competition

Key Terms & Definitions

Monopolistic Competition

A market structure with many sellers offering differentiated products.

- •Characteristics: Relatively large number of sellers, easy entry and exit, non-price competition (advertising).

- •Products are substitutes but not identical (e.g., fast food, furniture).

Product Differentiation

Strategies used by firms to distinguish their products from competitors, such as branding, quality, or features.

- •Gives the firm some control over price (Demand is downward sloping but highly elastic).

Long-Run Equilibrium (Monopolistic Competition)

In the long run, firms enter or exit until economic profit is zero.

- •Entry/Exit shifts the Demand curve.

- •Equilibrium: Price = ATC (Normal Profit), but Price > MC (Inefficient).

- •Demand is tangent to the ATC curve.

Excess Capacity

The gap between the minimum ATC output and the profit-maximizing output.

- •The firm could produce at a lower cost but holds back production to maximize profit.

4.5 - Oligopoly and Game Theory

Key Terms & Definitions

Oligopoly

A market structure dominated by a few large producers.

- •Characteristics: High barriers to entry, identical or differentiated products.

- •Key Feature: Mutual Interdependence (decisions depend on competitors).

Game Theory

The study of how people/firms behave in strategic situations.

- •Used to analyze the pricing and output decisions of oligopolies.

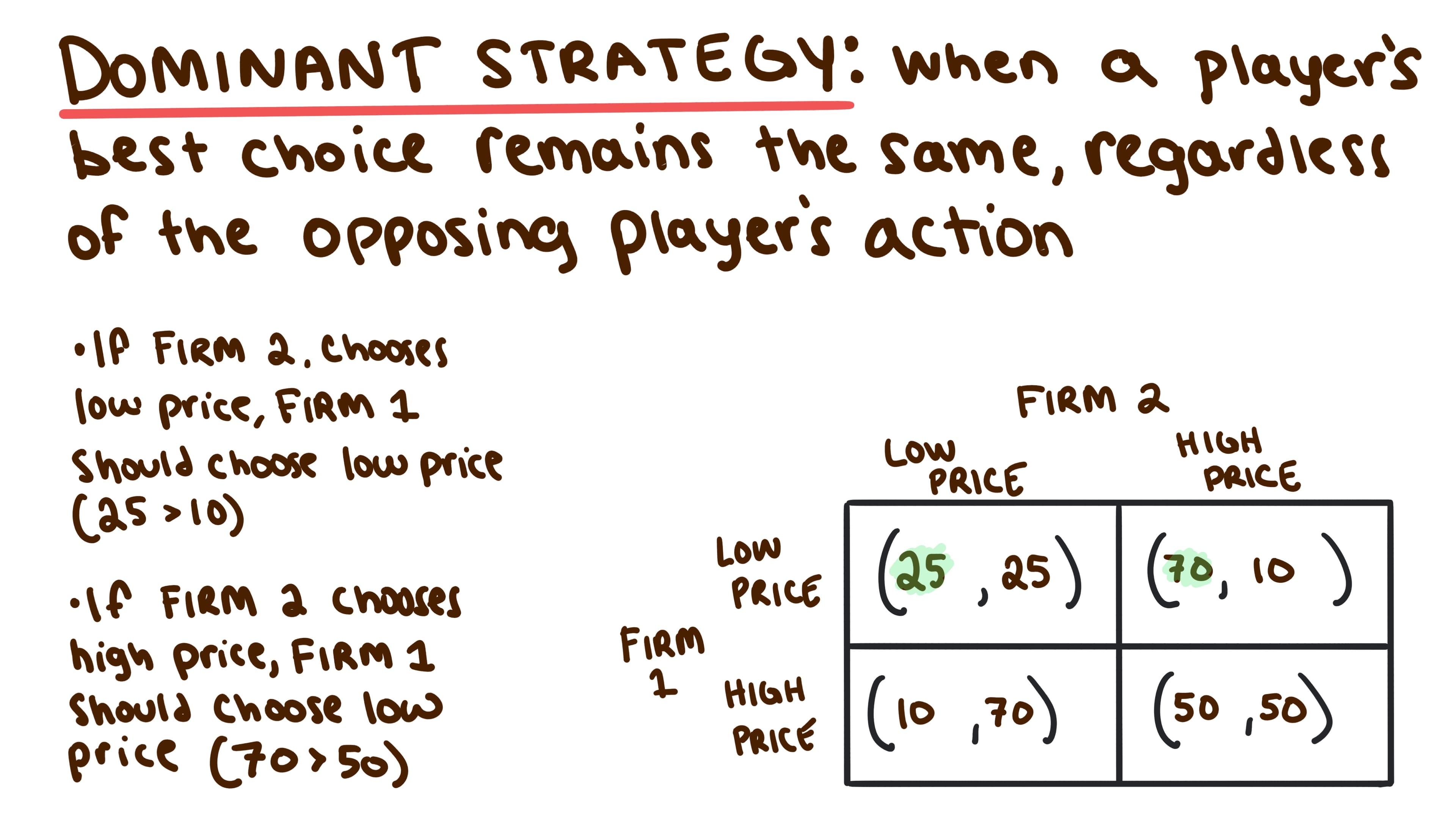

Dominant Strategy

The best move to make regardless of what your opponent does.

- •Not all games have a dominant strategy.

- •How to identify:

- •For Player 1: Check each row - if one row has higher payoffs than another in every column, that row is dominant.

- •For Player 2: Check each column - if one column has higher payoffs than another in every row, that column is dominant.

- •A strategy is dominant if it yields a better payoff than all other strategies, regardless of opponent's choice.

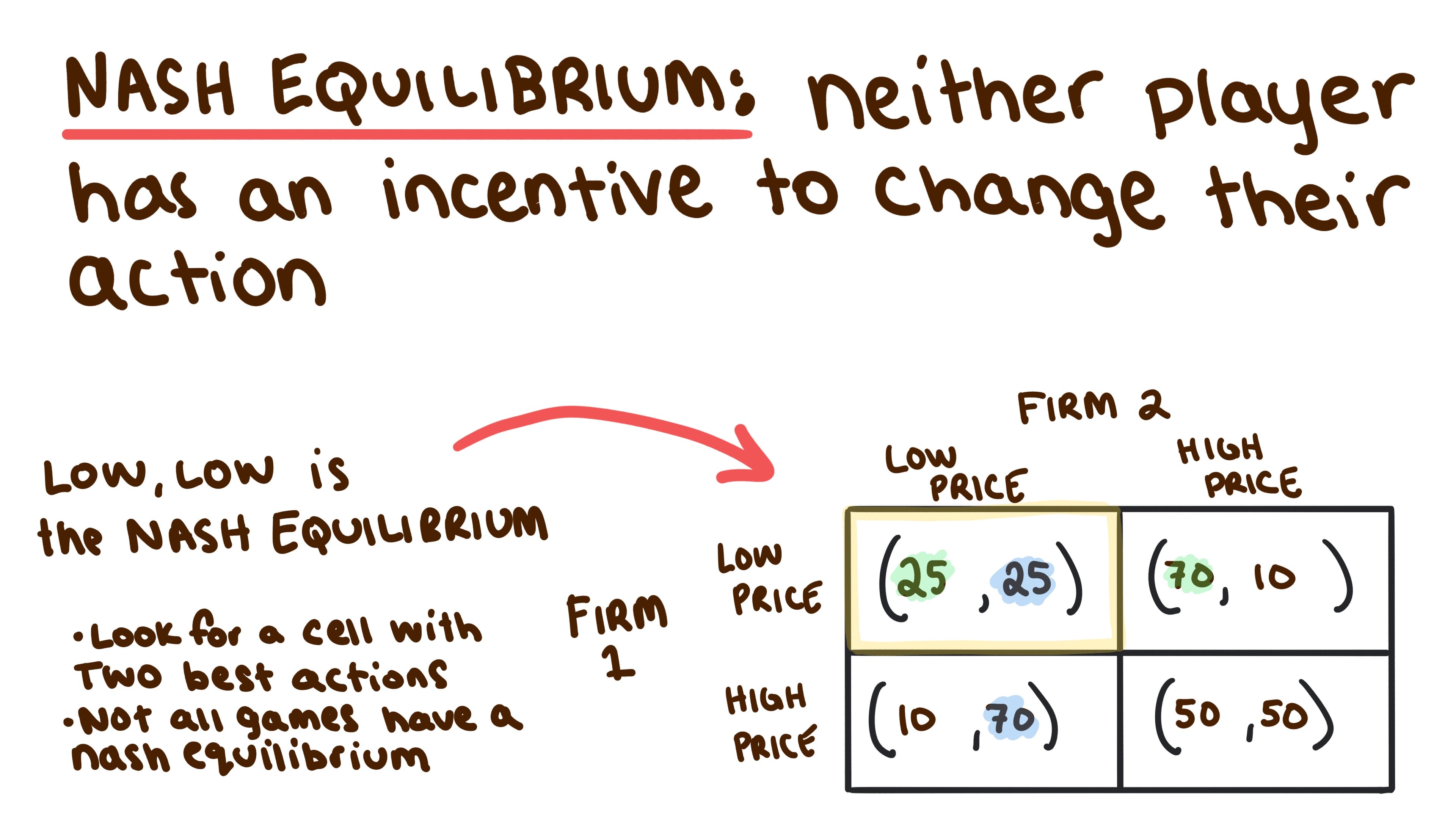

Nash Equilibrium

The outcome that occurs when both firms make decisions simultaneously and have no incentive to change.

- •The "optimal" outcome given the rival's choice.

- •How to identify:

- •Step 1: For each cell, check if Player 1's payoff is the highest in that column (best response to Player 2's strategy).

- •Step 2: For the same cell, check if Player 2's payoff is the highest in that row (best response to Player 1's strategy).

- •If both conditions are true, that cell is a Nash equilibrium.

- •A Nash equilibrium can exist even if neither player has a dominant strategy.

Collusion / Cartel

A group of producers that create an agreement to fix prices high, effectively acting as a monopoly.

- •They restrict output to maximize collective profit.

- •Cartels are unstable because firms have an incentive to cheat (lower price) to gain market share.

4.6

Whiteboards

Checkpoint

Test your understanding of 4.4

Monopolistic competition is characterized by:

Checkpoint

Test your understanding of 4.5

In game theory, a Nash equilibrium occurs when: